Municipals were steady to firmer in spots to close out August as inflows returned to muni mutual funds. U.S. Treasury yields fell and equities were mixed ahead of Friday’s employment report.

Triple-A benchmarks were bumped up to three basis points, depending on the scale, while UST yields fell three to four basis points.

The two-year muni-to-Treasury ratio Thursday was at 65%, the three-year at 66%, the five-year at 68%, the 10-year at 72% and the 30-year at 92%, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the two-year at 64%, the three-year at 66%, the five-year at 66%, the 10-year at 69% and the 30-year at 91% at 4 p.m.

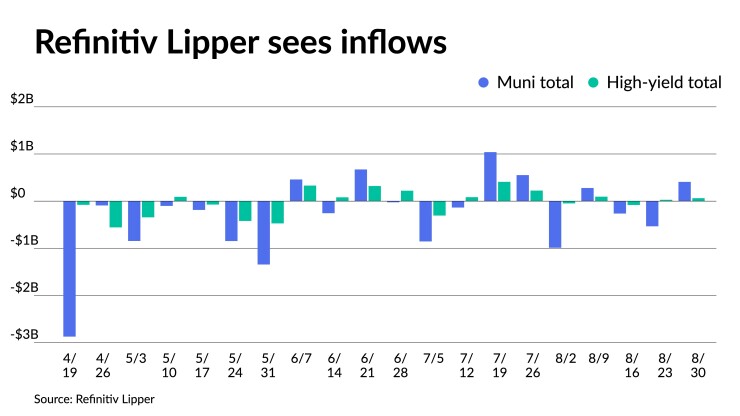

Refinitiv Lipper reported $407.976 million of inflows from municipal bond mutual funds for the week ending Wednesday after $534.428 million of outflows into the funds the previous week.

The tone and climate of the municipal arena were positive on Thursday as the market prepared to bid farewell to summer ahead of the long Labor Day holiday weekend.

“The market is quiet with a firm tone, however, there are not enough trades to point to,” a New York trader said on Thursday.

“Quiet but constructive tone, with prices steady” is how Michael Pietronico, chief executive officer of Miller Tabak Asset Management, described the market Thursday.

“Expectations for next week are neutral as the shortened week should usher in minimal volatility,” he said.

Next week will have a constructive tone, said Pat Luby, a CreditSights strategist, as a fair amount of redemption money will be available to investors Friday.

On Friday, $21 billion of principal and interest will be paid out, consisting of $15 billion of principal and $6 billion of interest, Luby said.

California will see the largest principal payouts with $3.7 billion, followed by Texas with $1.4 billion and Georgia with $1.3 billion, he noted.

“So that money should be burning a hole in investors’ pockets on Tuesday when they come back,” he said.

The positive tone is largely due to market-friendly data pointing to more subdued economic growth, according to Jeff Lipton, head of municipal credit and market strategy at Oppenheimer & Co., who said municipals were on firm ground along the curve starting Wednesday.

Overall, market technicals were pointing to good participation before trading halted ahead of Labor Day.

“Institutional buyers have money to put to work and we are seeing particular activity along the first 10 years of the curve,” Lipton said. “Although the new-issue competitive market began the week with a cheaper bias, mid-week revealed noted strength with better support.”

For much of the August selloff, he said municipals displayed “performance anxiety” with the asset class now significantly underperforming U.S. Treasuries.

Ratios are relatively attractive in the secondary given the underperformance, according to Lipton.

On the retail front, mom-and-pop investors are preferring the “4% parish structures and 5% coupon, good quality, with a low dollar price and 4.40%-plus yield to maturity,” he noted.

“This environment should cultivate more retail interest with sidelined cash being more actively invested,” Lipton added.

In August, “the tax-exempt market was somewhat just starved for bonds,” said Wesly Pate, senior portfolio manager at Income Research + Management. “The lack of supply is really starting to weigh on many factors.”

“Whenever we’re seeing pressures in other asset classes, they’re not quite reverberating into the municipal class, just given the fact that overall market turnover is a little bit subdued just because of the lack of supply,” he said.

That is starting to dampen overall volatility, and keeping things a bit more range-bound than what they normally would be, Pate noted.

That lack of supply in August, down 13% from 2022, has reduced the amount of turnover in the market.

“As market participants are looking at bond availability, they’re saying, ‘Well, if there are fewer bonds to choose from, I’m not going to sell bond A in the hopeful desire to replace it with bond B because the availability of bond B is becoming incrementally less certain,'” he said.

That is starting to have a meaningful impact on the market in terms of valuations and overall trading activity, he said.

But overall, Pate said August has seen a “rather tame environment.”

“Most recently, we’ve settled into a level of rates and that’s starting to give a little bit more transparency into what the future looks like, and that’s given the market a lot of confidence going forward,” he said.

With fund flows not being “meaningful” in either direction, Pate said “it’s going to be a supply picture in terms of the technical environment.”

Whenever there is growing demand but “limited supply and actually reduced supply, and we look compared to the last couple of years, technicals are arguably what’s driving the market.”

With August over, others looked toward the fourth quarter with optimism.

“We are hoping September is better than August, which underperformed Treasuries,” a New York trader said. “September and October are much softer reinvestment months, so we don’t expect a strong municipal market if supply picks up,” he said.

The 30-day Bond Buyer visible supply stands at $9.6 billion.

“Technicals should be constructive throughout September,” he said. “We are not ruling out momentary weakness, but we do think that munis are poised for better performance, and at current nominal yields, they offer attractive income opportunities against a favorable credit backdrop,” Lipton said.

In September, issuance will ramp up, according to Luby.

Next week will see a $2.6 billion California GO deal, which will do “pretty well.” In two weeks, he said the new-issue calendar will pick up even more with several large deals already on the schedule.

Secondary trading

Washington 5s of 2024 at 3.28%. Ohio 5s of 2024 at 3.32% versus 3.37%-3.32% Wednesday. Maryland 5s of 2025 at 3.14%.

NYC 5s of 2027 at 2.97%. LA DWP 5s of 2029 at 2.72%. Connecticut 5s of 2030 at 2.99%.

Minnesota 5s of 2032 at 2.94% versus 3.03%-3.00% Tuesday and 2.74% original on 8/15. Tennessee 5s of 2033 at 3.01%-2.83% versus 3.05% on 8/21 and 2.97%-2.95% original on 8/16. DASNY 5S OF 2035 AT 3.25%-3.24% versus 3.31%-3.32% on 8/24 and 3.23%-3.22% on 8/17.

Washington 5s of 2046 at 4.03%-4.05% versus 4.06% Tuesday and 4.08% on 8/23. Harris County, Texas, 5s of 2048 at 4.14% versus 4.09%-4.08% on 8/15 and 4.06%-4.01% original on 8/9.

AAA scales

Refinitiv MMD’s scale was unchanged: The one-year was at 3.25% and 3.14% in two years. The five-year was at 2.88%, the 10-year at 2.93% and the 30-year at 3.88% at 3 p.m.

The ICE AAA yield curve was bumped two to three basis point: 3.24% (-3) in 2024 and 3.17% (-3) in 2025. The five-year was at 2.84% (-3), the 10-year was at 2.83% (-3) and the 30-year was at 3.85% (-2) at 4 p.m.

The S&P Global Market Intelligence (formerly IHS Markit) municipal curve was unchanged: 3.26% in 2024 and 3.14% in 2025. The five-year was at 2.89%, the 10-year was at 2.94% and the 30-year yield was at 3.87%, according to a 4 p.m. read.

Bloomberg BVAL was bumped one to two basis points: 3.23% (-2) in 2024 and 3.14% (-1) in 2025. The five-year at 2.85% (-1), the 10-year at 2.85% (-1) and the 30-year at 3.84% (-1) at 4 p.m.

Treasuries were firmer.

The two-year UST was yielding 4.852% (-4), the three-year was at 4.541% (-4), the five-year at 4.236% (-4), the 10-year at 4.092% (-3), the 20-year at 4.393% (-3) and the 30-year Treasury was yielding 4.201% (-3) near the close.

Mutual fund details

Refinitiv Lipper reported $407.976 million of inflows from municipal bond mutual funds for the week ending Wednesday following $534.428 million of outflows the week prior.

Exchange-traded muni funds reported inflows of $759.794 million versus $105.005 million of outflows in the previous week. Ex-ETFs muni funds saw outflows of $351.818 million after $429.422 million outflows in the prior week.

Long-term muni bond funds had $676.451 million of inflows in the latest week after outflows of $297.863 million in the previous week. Intermediate-term funds had $50.794 million of outflows after $72.381 million of outflows in the prior week.

National funds had inflows of $522.487 million versus $496.381 million of outflows the previous week while high-yield muni funds reported inflows of $62.681 million versus inflows of $28.271 million the week prior.